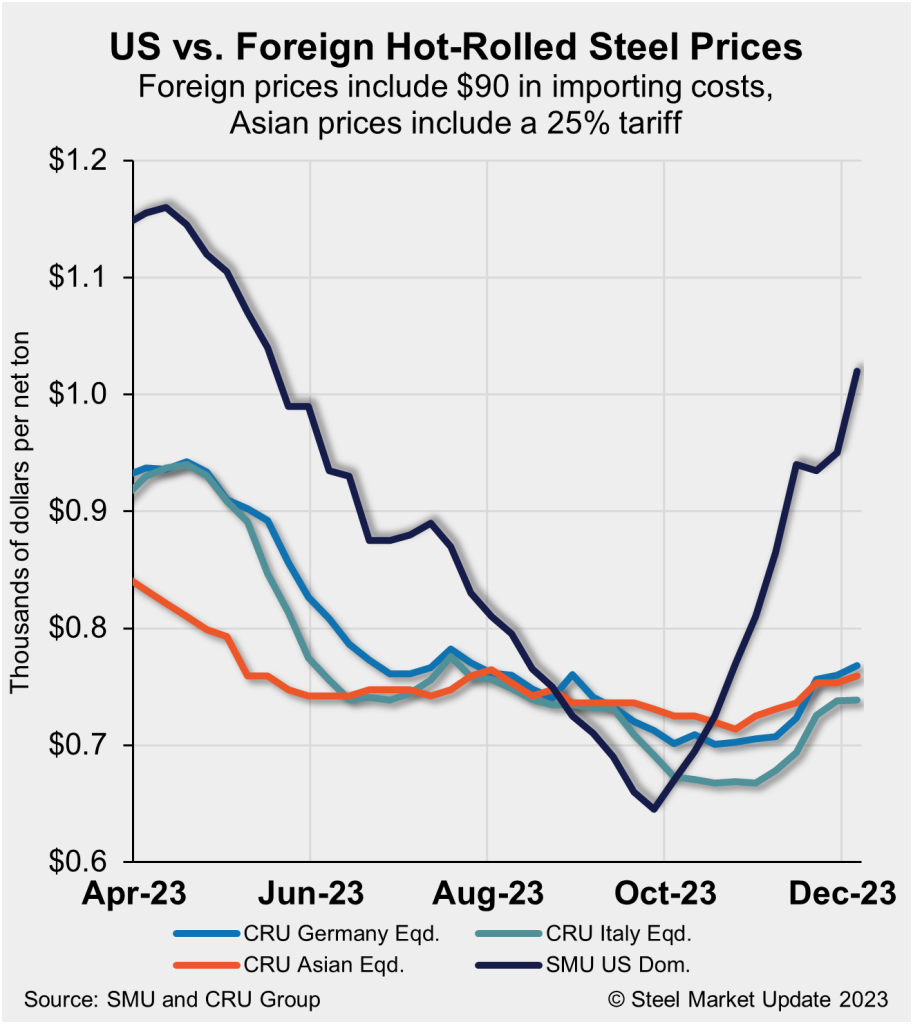

Currently, US hot-rolled coil (HRC) prices are notably lower than those in the EU, specifically Germany and Italy. As of late June 2024, domestic US HRC is approximately $36 per short ton cheaper than imported HRC from both Germany and Italy, and around $27 cheaper than Asian imports. This price disparity is influenced by factors such as regional demand, import costs, and strategic pricing by domestic mills in response to market conditions.

The global steel market presents a complex mosaic of regional dynamics, with varying economic landscapes shaping the pricing of Hot-Rolled Coil (HRC), a crucial benchmark in the steel industry. A stark contrast has emerged recently between the United States and the European Union, particularly Germany and Italy, in the pricing trends of HRC. This article delves into a detailed regional price comparison of steel coils, examining the factors contributing to the observed price differentials and analyzing the implications for both buyers and the steel industry at large.

Divergent Market Paths: US Downward Trend vs. EU Stability

The Hot-Rolled Coil markets in the United States and key European economies like Germany and Italy are currently charting distinctly different courses. In the US, the HRC market is characterized by a pronounced downward trajectory, with prices experiencing a significant decline to levels unseen in nearly two years. This price erosion has enhanced the competitiveness of domestically produced US HRC against imports, leading to a notable shift in market dynamics. Conversely, the German HRC market has demonstrated remarkable resilience, maintaining price stability even amidst subdued trading activity.

The pricing pressure in the US market is further evidenced by the narrowing spread between HRC and prime scrap prices, reaching a three-year low. This compression suggests potential strain on the profit margins of steel mills. Despite these challenging pricing conditions, the US steel industry has shown pockets of resilience, with raw steel mill production increasing by 4% in May, indicating a degree of sustained or potentially improving demand.

Recent data from late June 2024 reveals that US domestic HR coil tags averaged $670 per short ton (st), a further decrease from previous weeks. This decline positions domestic HRC at a 5% discount compared to import prices, a widening gap from previous weeks and marking a nine-month low from a recent peak in April. Industry analysts suggest that while further price reductions in cold-rolled and coated steel are possible, the downside risk for HRC prices may be limited, as mills might already be operating near or below breakeven points.

In contrast to the US market’s downward pressure, the German HRC market has exhibited stability. Throughout July, prices have largely remained unchanged, despite an environment of muted trading. This stability exists in a market characterized by oversupply and weak demand, with buyers holding adequate inventories and demonstrating limited urgency for new acquisitions. While the broader European HRC market anticipates potential price softening in August, particularly in Southern Europe, expectations lean towards a recovery post-summer, albeit a slow one due to limited overall end-user demand.

Import dynamics also diverge significantly between the regions. In the US, decreasing domestic prices and shorter lead times are expected to curtail import volumes, potentially offering some support to domestic HRC prices in the coming weeks. Conversely, import offers in Germany have been scarce, with major Asian suppliers having largely fulfilled their third-quarter delivery quotas. New EU import safeguards further contribute to a subdued import market in Europe.

Price Comparison Table: USA vs. EU Hot-Rolled Coil (HRC)

| To clearly illustrate the price differences, the following table compares HRC prices and related factors in the US, Germany, and Italy, based on available data from late June and early July 2024: | Region | Domestic HRC Price (per short ton) | Import HRC Price (Delivered to US port, est.) | Premium/Discount vs. Imports | Key Market Trend | Factors Influencing Price |

|---|---|---|---|---|---|---|

| USA | $670 | See below | Downward Trend | Weak demand, competitive pricing, decreasing imports |

| Germany (EU) | ~$616 (CRU Price, needs import cost) | $706 (Estimated, incl. $90 import cost) | US is ~$36 Cheaper | Stable | Oversupply, subdued demand, import safeguards |

| Italy (EU) | ~$616 (CRU Price, needs import cost) | $706 (Estimated, incl. $90 import cost) | US is ~$36 Cheaper | Tentative Price Hikes | Subdued consumption, potential post-safeguard price hikes |

| Asia | ~$485 (CRU Price, needs tariff & cost)| $697 (Estimated, incl. 25% tariff & $90 cost)| US is ~$27 Cheaper | Volatile | Export challenges, domestic economic uncertainty in China |

Note: Import prices are theoretical calculations including estimated import costs and tariffs where applicable. Actual import costs can vary.

Decoding the Price Gap: Factors at Play

Several factors contribute to the price divergence between US and EU HRC markets:

1. Demand-Supply Dynamics: The US market is experiencing weaker demand relative to supply, compelling domestic mills to adopt aggressive pricing strategies to secure orders. Capacity expansions in the US further exacerbate this supply-demand imbalance. Conversely, while the EU market faces subdued demand, it also grapples with oversupply, yet prices have remained comparatively stable, potentially indicating a greater willingness of EU producers to manage supply or different cost structures.

2. Import Costs and Trade Policies: Import costs play a significant role in price differentials. The provided data includes an estimated $90 per short ton for freight, handling, and trader margin added to foreign HRC prices delivered to US ports. For Asian imports, a 25% tariff further inflates the delivered price to the US. While Section 232 tariffs no longer apply to most EU imports, new EU import safeguards and tariff rate quotas influence import volumes and market dynamics within the EU. These trade policies directly impact the competitiveness of imported steel and influence domestic pricing strategies.

3. Regional Economic Conditions: Differing regional economic landscapes also contribute to price variations. The US market reflects its own unique economic pressures and industry-specific challenges, distinct from those in the Eurozone. Factors such as automotive and construction sector demand within each region, broader macroeconomic trends, and industrial recovery rates all play a role in shaping steel demand and pricing.

4. Strategic Pricing by Mills: US steel mills appear to be strategically pricing HRC to be competitive against imports, even at the potential cost of margin compression. This strategy is evident in the widened negative premium of US HRC compared to import prices. EU mills, particularly in Germany, may be adopting different strategic approaches, prioritizing price stability over aggressive volume sales in the current market environment.

5. Lead Times and Service: Domestic US steel offers shorter lead times compared to imports, a factor that can influence buyer decisions, particularly in dynamic market conditions. This advantage of quicker delivery can justify a premium for domestic steel in some circumstances, but currently, US mills are leveraging it to offer more competitive pricing overall.

Implications and Future Outlook

The current price disparity between US and EU steel coils has significant implications for buyers and the industry:

- For US Steel Buyers: Lower domestic HRC prices present a cost advantage for US manufacturers and industries relying on steel inputs, enhancing their competitiveness. The increased price gap between domestic and imported steel further incentivizes domestic sourcing.

- For EU Steel Buyers: Comparatively higher and more stable HRC prices in the EU mean higher input costs for European manufacturers. The anticipation of post-summer recovery and potential price increases adds to cost management considerations for EU buyers.

- For Steel Producers: US steel mills are facing margin pressures due to lower prices, necessitating efficient operations and strategic cost management. EU mills, while maintaining price stability, must navigate oversupply and subdued demand, awaiting a potential market recovery.

Looking ahead, the outlook for HRC prices in both regions remains subject to evolving market conditions. In the US, while some analysts suggest limited further downside for HRC prices, the market will closely monitor demand recovery and raw material price trends. Potential stabilization is anticipated as import competition eases. The EU market, particularly Germany, is expected to maintain near-term price stability, with cautious optimism for a gradual post-summer recovery contingent on demand increases and the effectiveness of trade measures.Conclusion: Navigating a Dynamic Steel Landscape

The regional price comparison of steel coils between the US and EU reveals a market characterized by divergent trends and influenced by a complex interplay of factors. While the US HRC market currently offers more competitive prices driven by downward trends and strategic mill pricing, the EU market, particularly Germany, demonstrates stability amidst oversupply and subdued demand. Factors such as demand-supply dynamics, import costs and trade policies, regional economic conditions, and mill strategies all contribute to the observed price differentials. As both markets navigate these complexities, stakeholders must remain vigilant and adaptive, recognizing the dynamic nature of the global steel landscape and the critical interplay between domestic and international influences on HRC pricing. The contrasting market conditions in the US and EU underscore the importance of regional analysis in understanding global steel market trends and making informed business decisions.